Skip to presentation

OJ

Overjet

Case acceptance

01

Product assessment

Build the Case Acceptance Engine

02

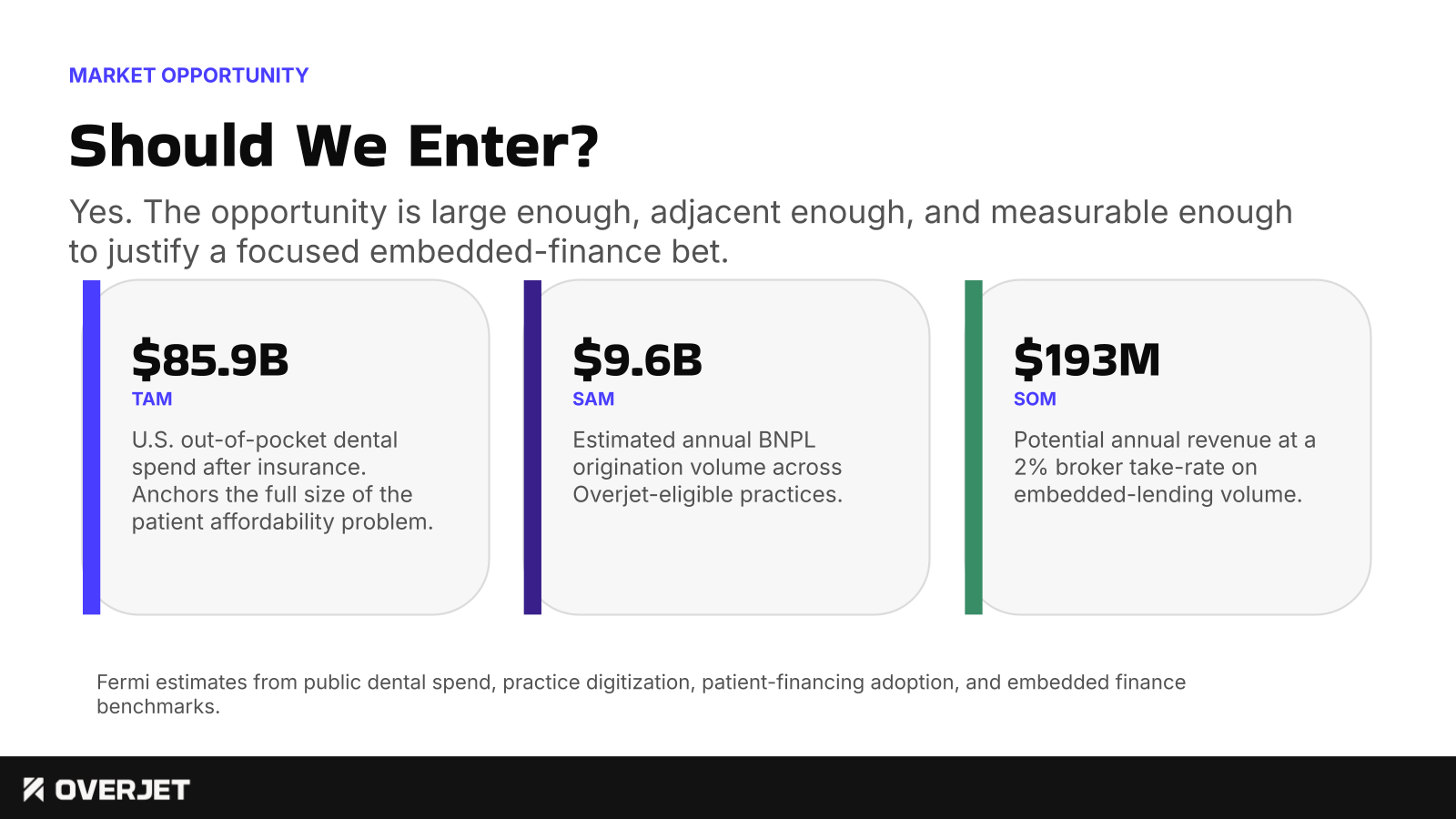

Market opportunity

Should We Enter?

03

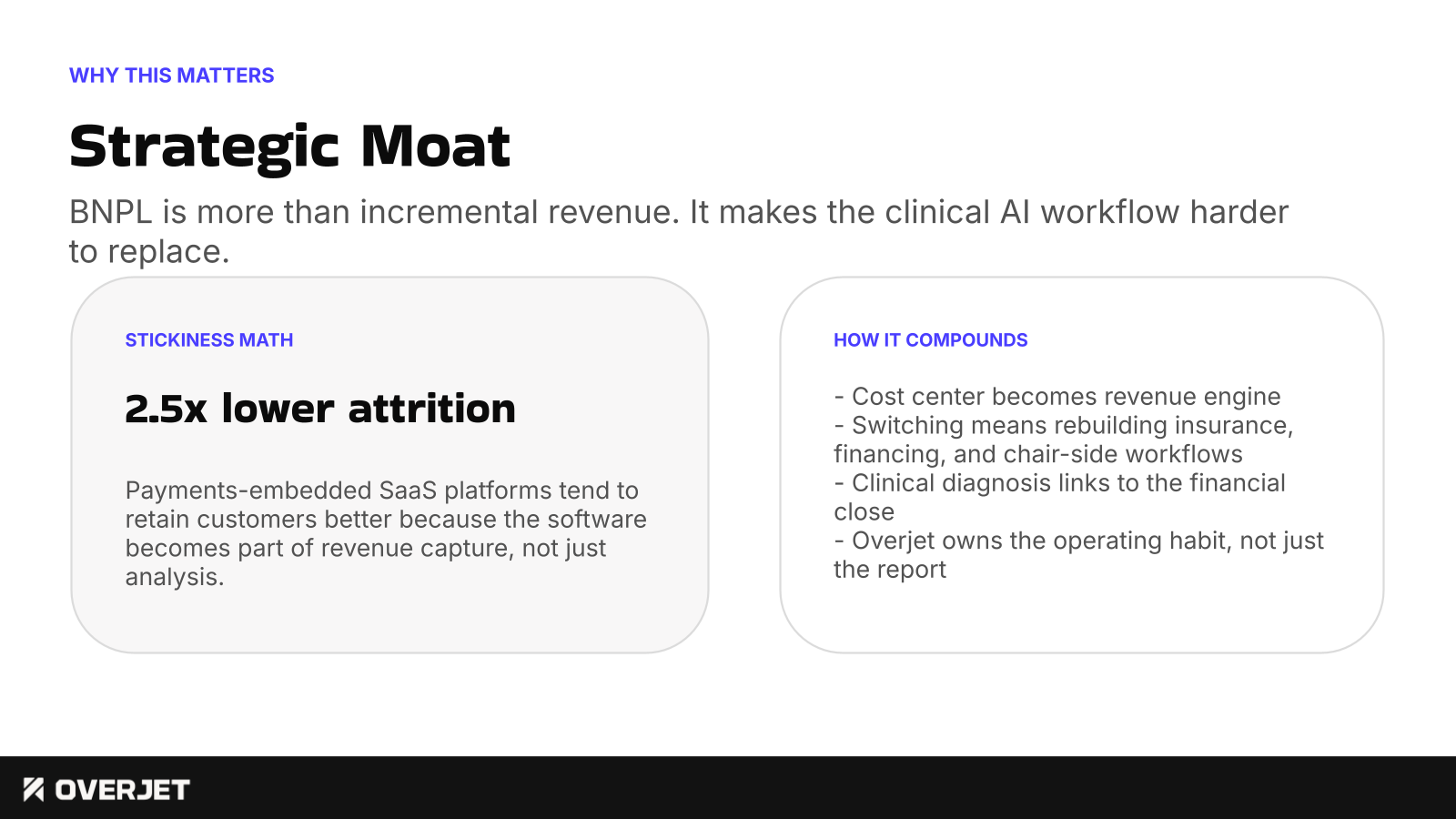

Why this matters

Strategic Moat

04

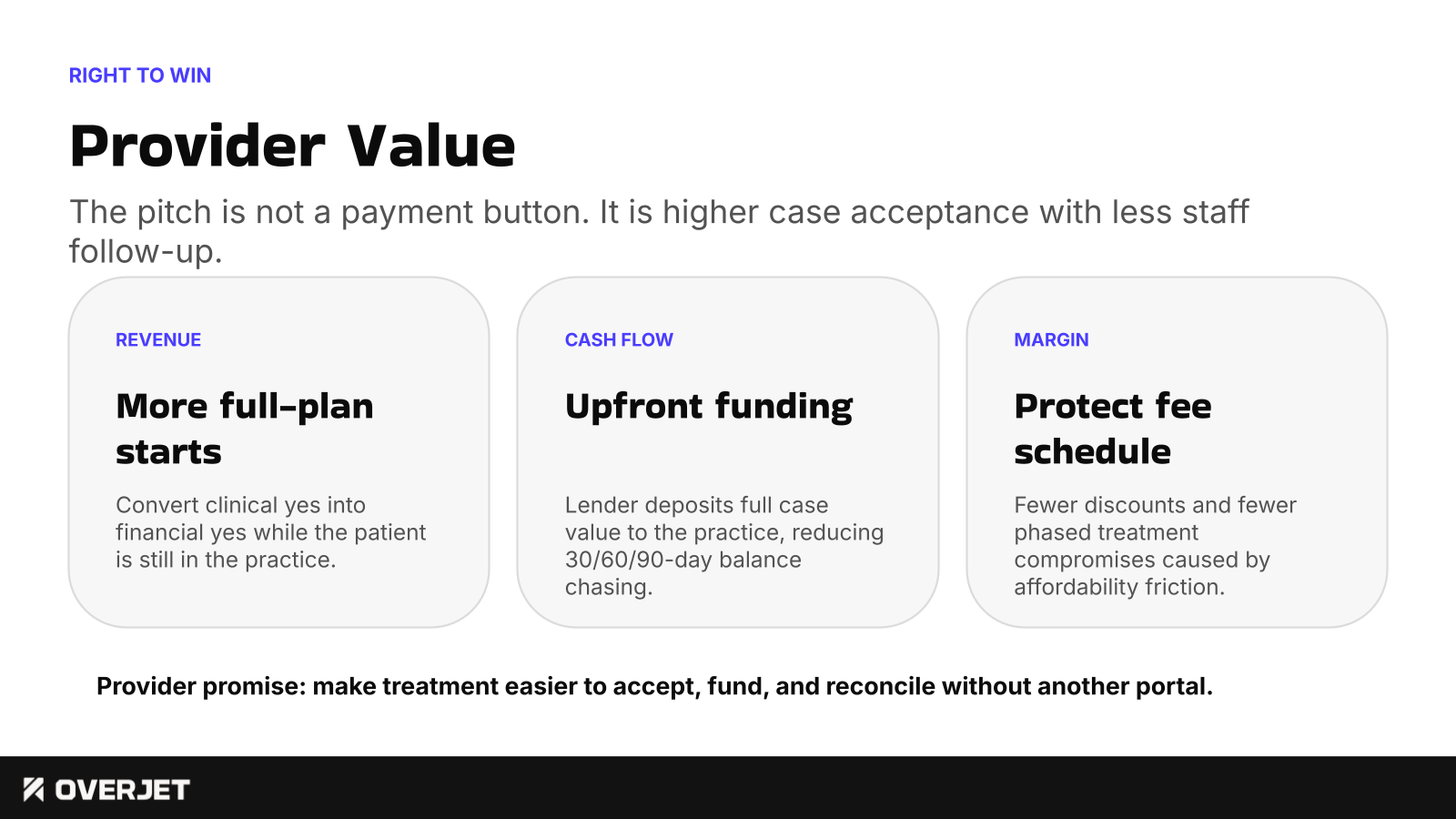

Right to win

Provider Value

05

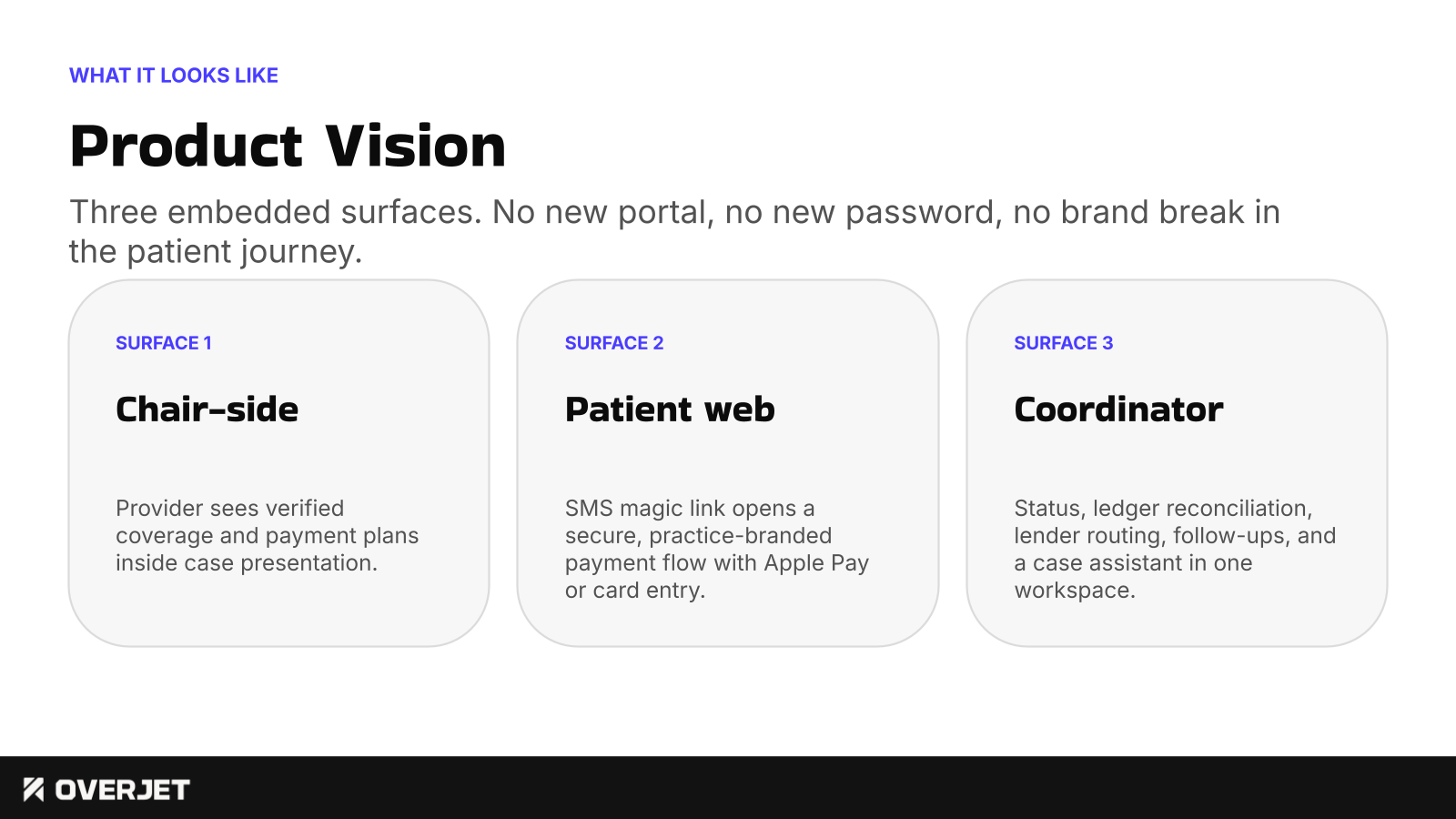

What it looks like

Product Vision

06

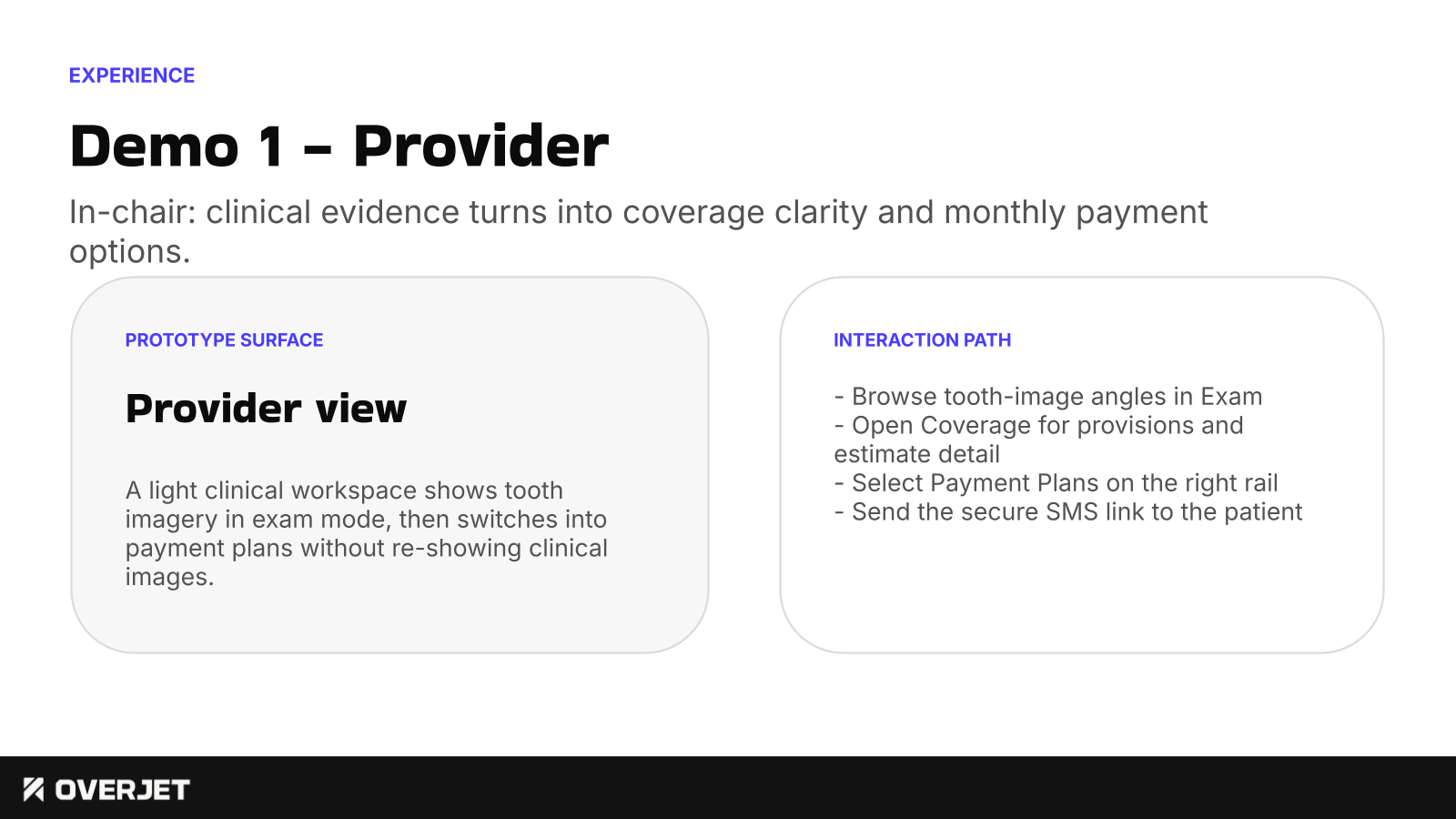

Experience

Demo 1 - Provider

07

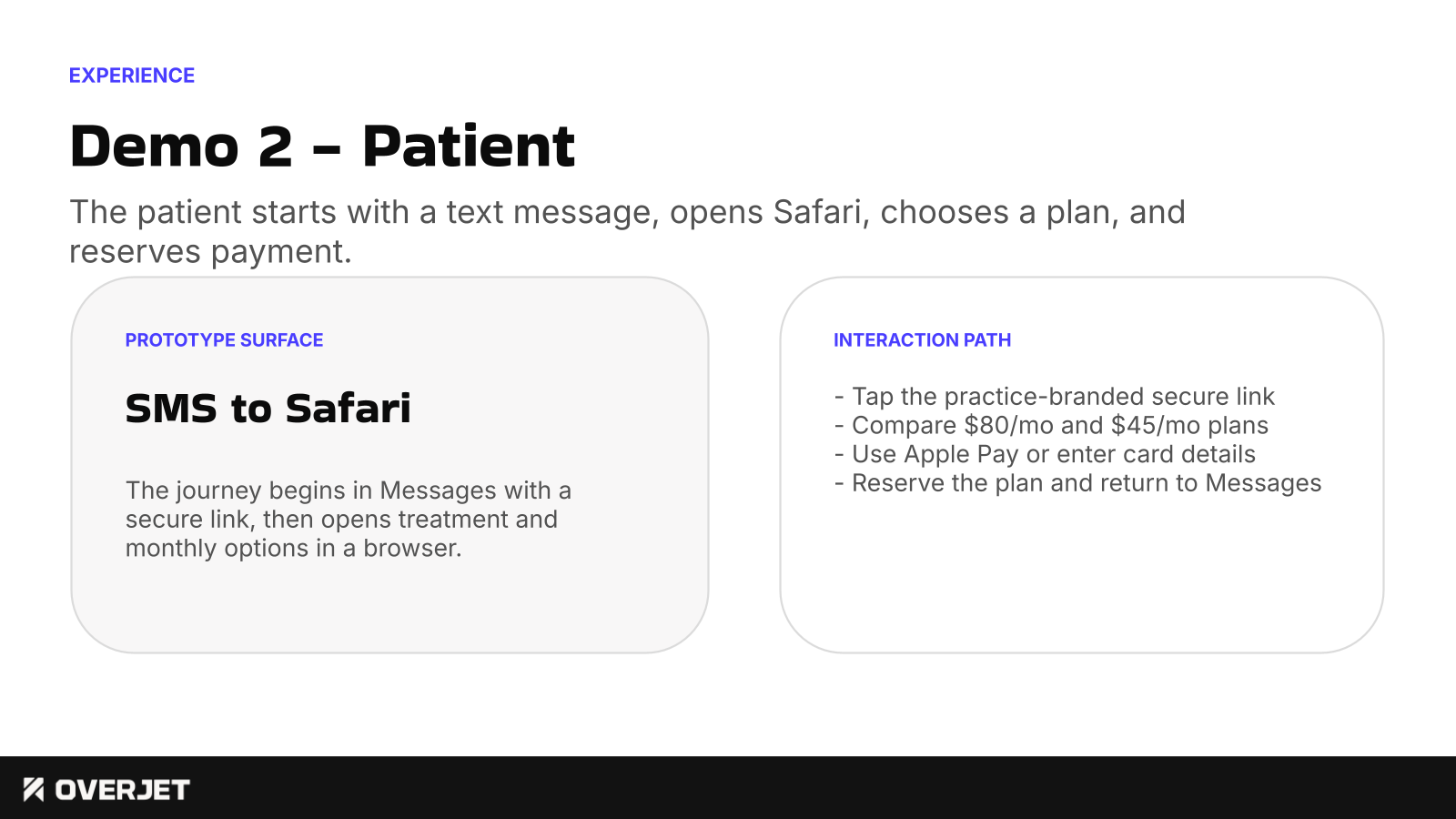

Experience

Demo 2 - Patient

08

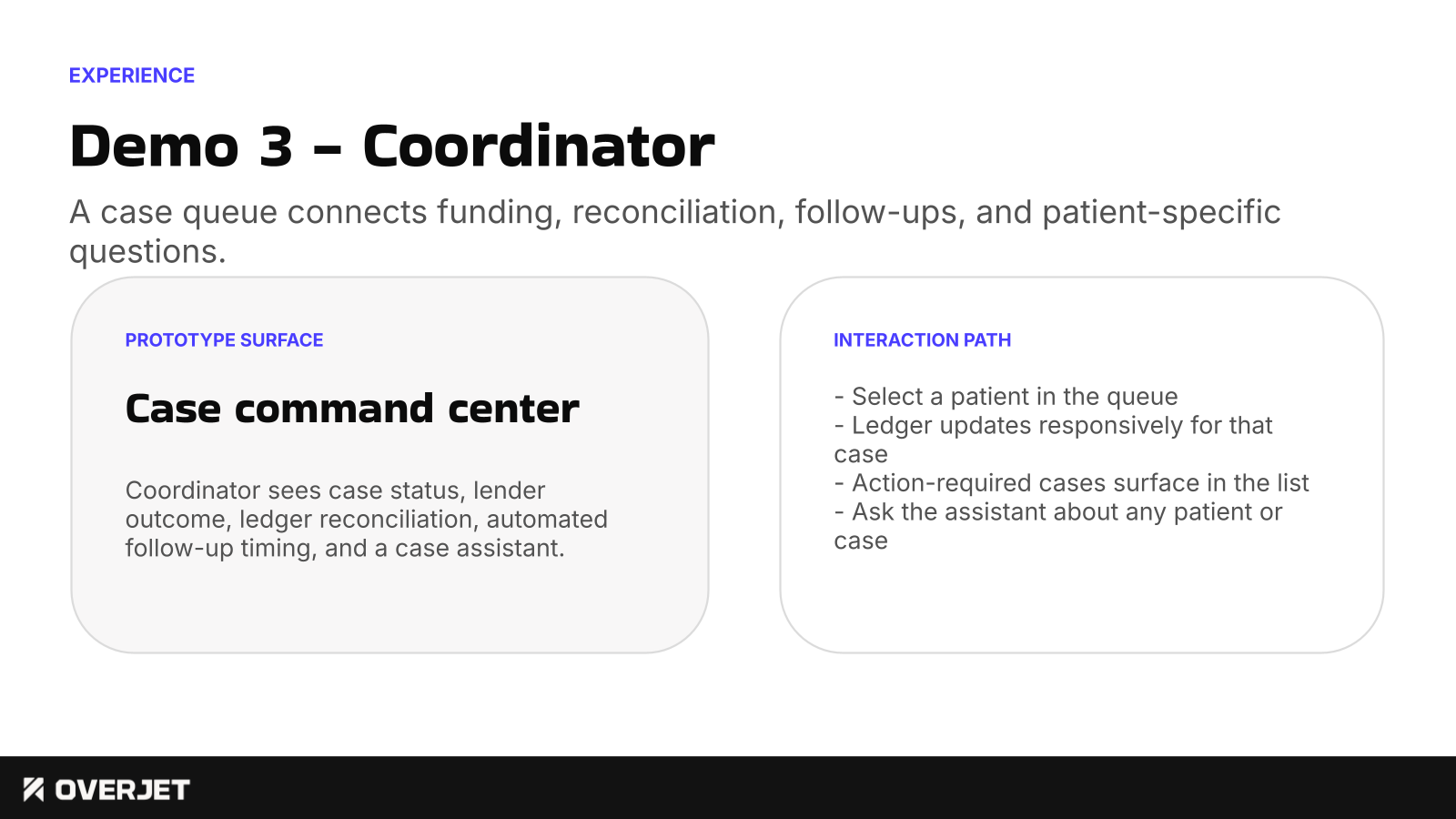

Experience

Demo 3 - Coordinator

09

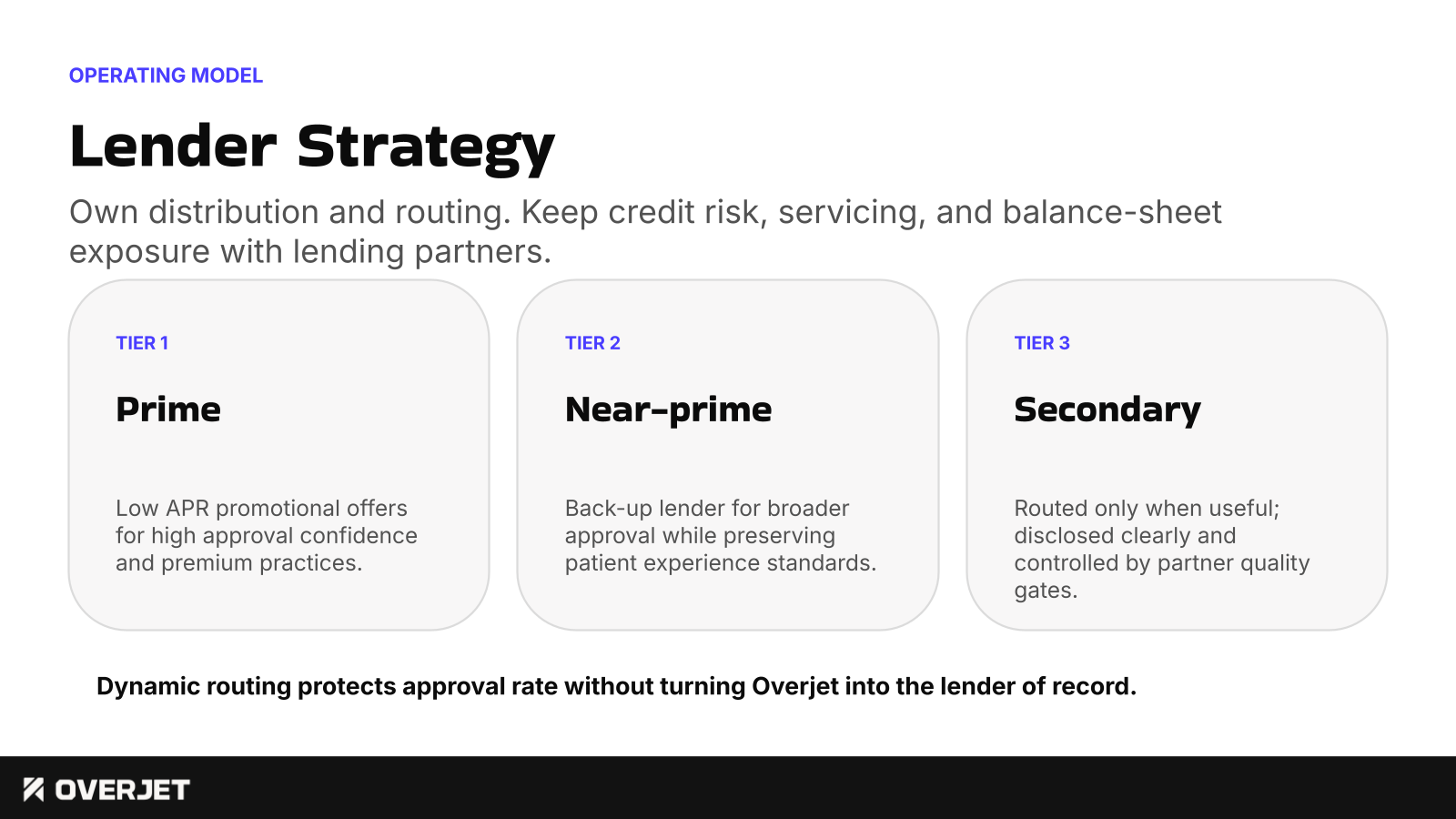

Operating model

Lender Strategy

10

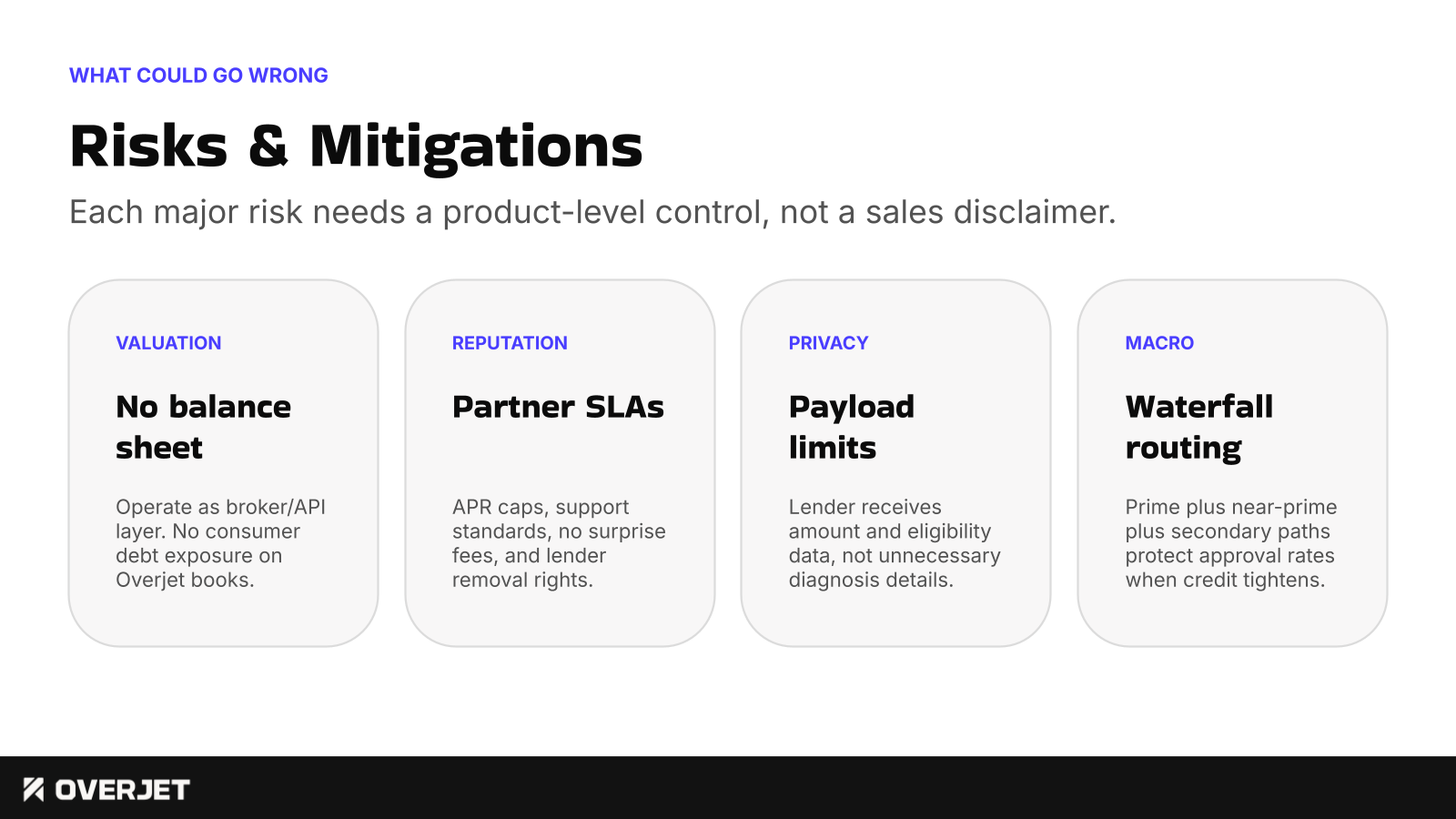

What could go wrong

Risks and Mitigations

11

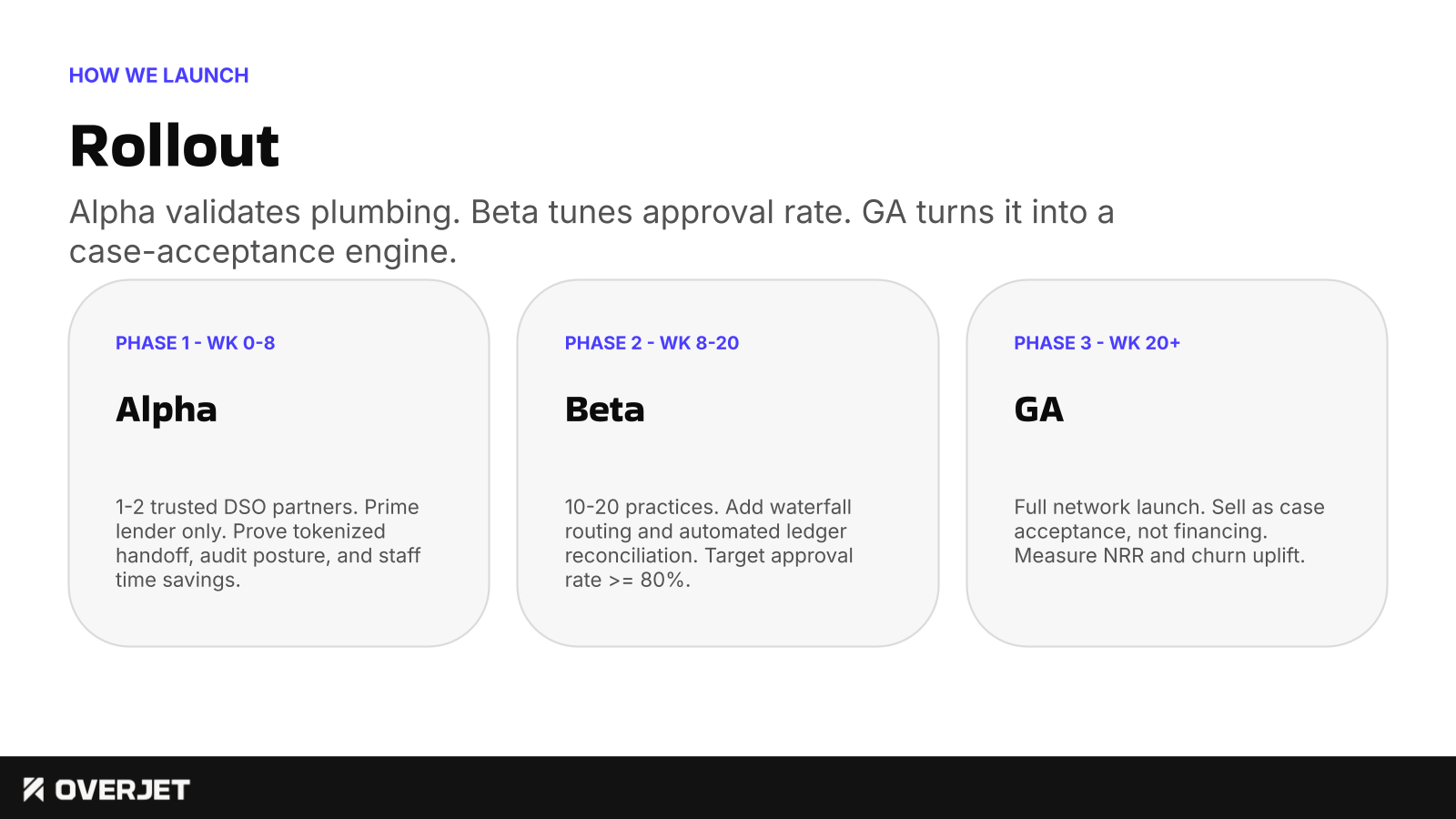

How we launch

Rollout

12

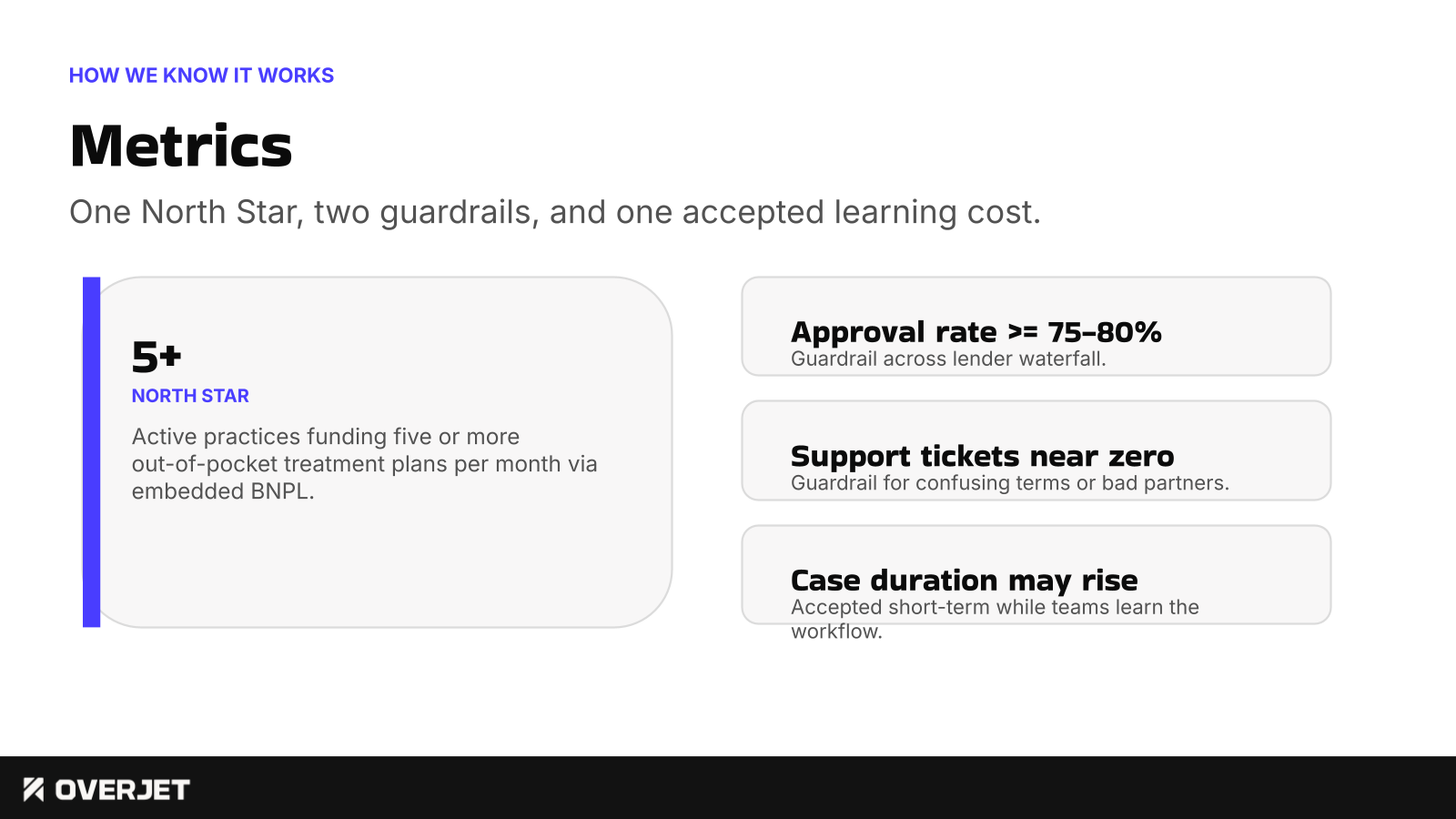

How we know it works

Metrics

13

References

Appendix